Prediction markets are booming. Oversight is barely there.

Prediction markets once lived on the academic fringe. Now they’re trading billions on politics, sports, and celebrity gossip — under rules never designed for retail gamblers.

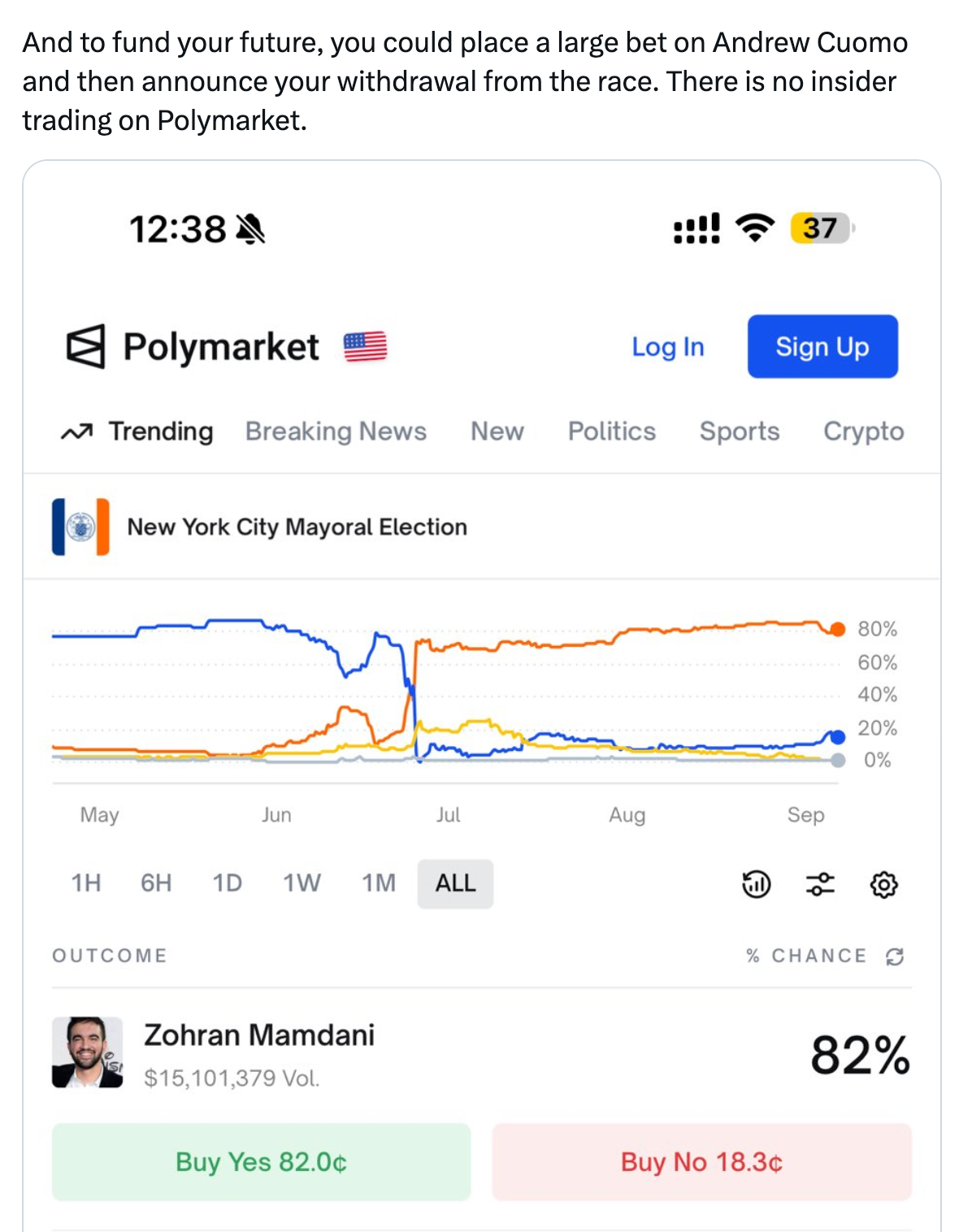

When billionaire Bill Ackman suggested on Twitter that Eric Adams could “place a large [Polymarket] bet on Andrew Cuomo and then announce [his] withdrawal” from the New York City mayoral race, he described something that feels profoundly illegal. A politician profiting from non-public knowledge of their own withdrawal from an election surely crosses some line — insider trading? Market manipulation? Election interference? Illegal gambling? Ackman ended his tweet: “There is no insider trading on Polymarket”1 — not because it doesn’t happen, but because it won’t be charged. He’s right: the Securities and Exchange Commission’s insider trading rules don’t apply here. But that leaves the question: what rules, if any, do?

As Ackman says, prediction markets fall outside the SEC’s jurisdiction,a living in a different regulatory world than stock markets where executives get prosecuted for trading on non-public earnings or tipping off friends about upcoming mergers. Unlike crypto’s ongoing turf wars between regulators, prediction markets have a clear home: the Commodity Futures Trading Commission, which oversees futures, swaps, and other derivatives trading. A farmer worried about a poor wheat harvest can buy futures contracts that rise in value if wheat prices increase, helping to offset the money lost from selling less grain. An airline can buy oil-based futures contracts to offset the risk of jet fuel costs rising, effectively letting them budget fuel at today’s prices even if market rates climb before delivery. Some derivatives markets more closely resemble prediction markets, dealing in events rather than commodities — for instance, ski resorts can hedge against poor snowfall by trading weather-based contracts.

While farmers hedging wheat prices serves a clear economic purpose, prediction markets operate in murkier territory. When people trade on sports games or celebrity relationships, are they engaging in legitimate derivatives trading deserving the same regulatory treatment? Or are platforms like Kalshi and Polymarket essentially gambling sites operating under the veneer of financial markets? And with participants potentially losing big money to better-informed insiders, who’s ensuring these markets stay fair? What happens when prediction markets collide with other issues — from market manipulation to gambling addiction to election integrity?

Citation Needed is an independent publication, entirely supported by readers like you. Consider signing up for a free or pay-what-you-want subscription.

The history of prediction markets

Prediction markets — platforms where people trade contracts that pay out based on whether specific events happen — have enjoyed a surge in popularity over the last few years as they’ve dramatically expanded their operations in the United States. While they have existed for decades, they were long confined to strictly academic exercises — operating as small-scale non-profits that carefully constrained their operations to avoid running afoul of the CFTC. The pioneers were university-affiliated non-profits like Iowa Electronic Markets, which capped trades at modest dollar amounts, and later PredictIt, which followed a similar model. The CFTC allowed their elections- and economy-related markets by issuing no-action letters, recognizing there was value in studying whether crowdsourcing predictions through financial markets could outperform traditional polling and forecasting methods.

In 2020, the US-based Polymarket began allowing customers to use cryptocurrency to trade events contracts, though they made no effort to certify their contracts with the CFTC. In 2021, Kalshi emerged as the first fully regulated prediction market in the US, following a hard-won CFTC approval. That platform allowed traders to stake up to $25,000 on outcomes ranging from COVID-19 vaccination rates to record-breaking temperatures.

The CFTC cracked down on prediction markets in 2022. First, they hit the unregistered Polymarket with a $1.4 million fine and ordered it to stop offering unregistered event contracts to US customers, effectively shutting the platform out of the American market.2 Then they revoked PredictIt’s no-action letter,3 apparently concluding the platform had expanded beyond its academic purpose into a commercial enterprise. PredictIt challenged this decision in court, winning a preliminary victory in 2023 and a final one in 2025. In 2023, the CFTC ordered Kalshi to stop offering markets on which party would control Congress after the upcoming elections, citing the Commodity Exchange Act’s prohibition on “gaming”. Kalshi also mounted an aggressive legal challenge, and when a district court ruled in Kalshi’s favor in 2024, the company swiftly reinstated the contested markets [I66].

The regulatory landscape shifted further after Trump took office. The CFTC’s interim leadership began championing prediction markets as “an important new frontier”,4 and dropped both their appeal in the Kalshi case and an ongoing investigation into Polymarket’s continued accessibility to US users [I89]. Polymarket acquired a CFTC-regulated derivatives exchange, and a no-action letter from the agency greenlighted their re-entry into the US [I92]. With the administration’s deregulatory stance and a nominee for CFTC Chair who sits on Kalshi’s board [I90], this permissive approach is likely to accelerate in the coming years. More companies are eager to join the fray, with Crypto.com, Robinhood, and even the sports betting company FanDuel adding event contracts to their offerings. Eyeing this lucrative market, they’re likely to follow their predecessors’ lead in pushing regulatory boundaries even if it means expensive litigation. Following the crypto industry playbook, they may also lobby Congress for special exemptions.

The regulatory landscape

The US financial regulatory landscape is divided among several agencies, with the Securities and Exchange Commission (SEC) overseeing stock markets and various other securities. The SEC aggressively pursues unlawful insider trading cases when people trade securities based on material non-public information. Former SEC official John Reed Stark explains, “The rationale for policing unlawful insider trading is that for the markets to work efficiently and fairly, everyone needs to be working with the same basic information, or at least, that those with special access to nonpublic information are prevented from taking advantage of it before other investors.”

But with the Commodity Futures Trading Commission (CFTC), which oversees prediction markets, it’s a different world. Trading based on non-public information is built into the system: a cattle rancher can use early calving data to hedge against future beef prices, even though others lack access to that information. Laurian Cristea, a lawyer specializing in financial services and CFTC exchanges, explains, “it’s not wrong to trade on information you properly know or developed through your business.” Nevertheless, rules against fraud or market manipulation still prohibit trading based on illegally acquired private information, or making false or misleading statements that impact markets, and CFTC-regulated exchanges like Kalshi are required to establish and enforce their own rules to maintain fair markets.

Some states and tribal governments have also brought cases against Kalshi under state or federal gambling laws, arguing that it is skirting licensing, tax, and consumer protection requirements that apply to sportsbooks and casinos. In court filings, Kalshi insists it’s not a casino or sportsbook but rather a venue for traders to engage in “legitimate hedging”, similar to how farmers and airlines use futures markets to manage risk. However, their public messaging tells a different story, with their advertising and social media regularly inviting customers to come “bet”.

When fighting the CFTC in court over their election-related markets in early 2024, Kalshi insisted that Congress’s “gaming” restrictions were aimed specifically at sports betting, not election predictions. Their lawyers argued, “‘sporting events such as the Super Bowl, the Kentucky Derby, and Masters Golf Tournament’ were precisely what Congress had in mind as ‘gaming’ contracts”.5 A year later, Kalshi launched markets on these very same sporting events.

Kalshi has since argued they can’t be classified as a gambling platform since traders bet against each other rather than against a “house”. Andrew Kim, a lawyer specializing in gaming law and contributor to the Event Horizon newsletter, acknowledges that some of Kalshi’s arguments against state gambling oversight may be valid under a strict reading of the law, but that this particular defense is weak. “There are a number of exchange wagering outlets... generally covered by state level gambling law.” He adds: “if you play poker, the house takes a rake, but it doesn’t participate. That’s still gambling.”

Kalshi has also argued that, as a CFTC-regulated Designated Contract Market, the Commodity Exchange Act gives the agency exclusive jurisdiction over its event contracts. This claim of federal preemption has been disputed by state gambling regulators, and courts have not yet resolved the question.

Old rules, new markets

Though prediction markets aren’t a new phenomenon, their growing accessibility to retail traders is. Unlike the SEC, which prioritizes protecting retail investors, the CFTC’s mandate is centered on market integrity and preventing fraud or manipulation — not on consumer protection. Its regulations were designed for businesses hedging wheat and oil, not retail traders betting on album releases and how many times Elon Musk tweets in a month. Is a regulatory framework designed for commercial hedgers adequate for these retail-heavy markets? Should regulators try to protect retail traders who are consistently outmaneuvered by insiders with private information or other participants with structural advantages?

Some experts think the CFTC’s oversight could work. Lee Reiners, a lecturing fellow at the Duke Financial Economics Center, explains that “any insider trading on these contracts would clearly implicate the anti-fraud provisions of the Commodity Exchange Act,” potentially triggering both CFTC enforcement action and a referral for criminal charges from the Department of Justice.

When I asked Cristea about the CFTC’s ability to oversee retail markets, he pointed to the CFTC’s track record regulating Futures Commission Merchants (FCMs), which facilitate trading of futures and derivatives. While institutional clients still dominate these markets, retail participation has grown significantly in recent years. However, he notes a key difference in consumer protections: “FCMs don’t have the same sort of requirement for a customer suitability analysis that applies to broker-dealers in the securities context.” Broker-dealers are obligated to assess whether specific investments are appropriate for specific customers. For example, if a 65-year-old retiree with limited savings tried to make a substantial investment in a high-risk stock, a broker-dealer would need to evaluate whether the investment suited her financial situation and could refuse inappropriate trades.

Cristea also expressed concerns about enforcement capacity. “The current administration takes a more free market, caveat emptor-type approach. That said, even when the CFTC got jurisdiction over a very large swaps market the agency’s budget was not increased much. And together with this deregulatory trend, agencies getting smaller in size, where agencies are being told to do more with less, I am not sure the CFTC will necessarily come out with [additional retail] protections unless the agency sees that as a necessary step for credibility and for the market to thrive.” The CFTC has yet to bring any enforcement actions pertaining to market manipulation on events contracts, and it’s not clear they have much appetite to begin doing so.

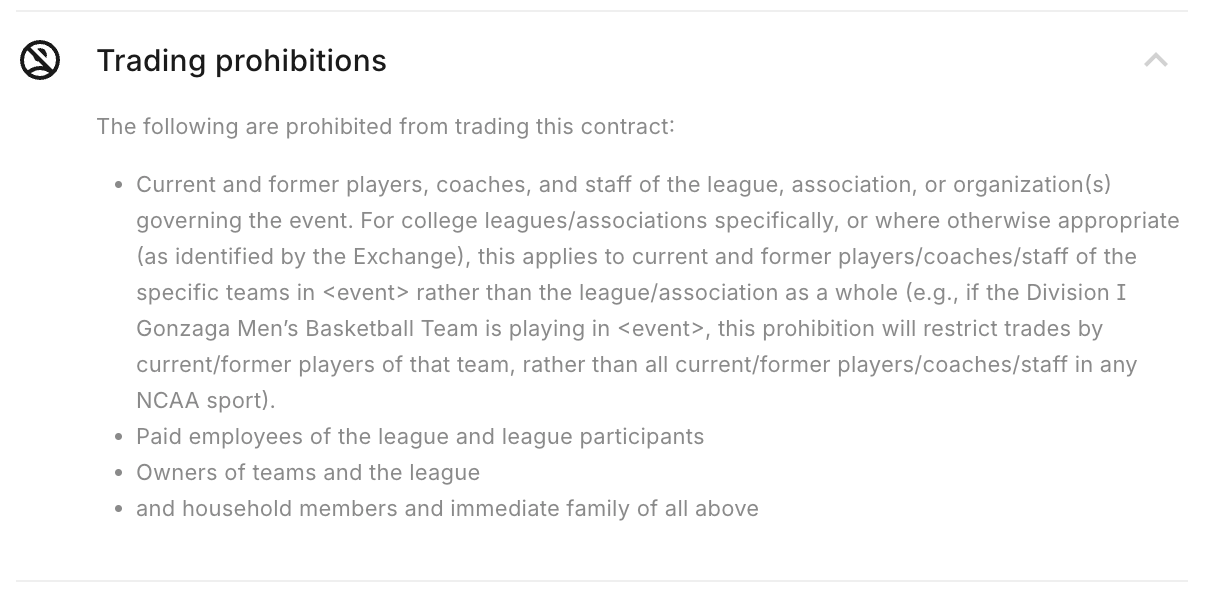

Other industries that deal with outcome-based bets, like sports wagering, have evolved robust integrity systems both to protect consumers and to preserve trust in the games themselves. Kim explains, “The reason for [these rules] is because of the mob, because of the history of gambling and the mob fixing matches. You have a rather sketchy history of criminal influence on the outcome of matches, and so you want to prevent that by just having very strict rules, like if you’re involved in the event, you can’t play, period.”

Today, sports betting platforms work to screen out athletes, referees, and sports program employees to ensure they’re not betting on games they could potentially influence, and employ monitoring programs to detect suspicious bets. This vigilance has proven effective: recent scandals involving illegal betting by Iowa State football staff and the University of Alabama’s baseball coach were first flagged by the platforms’ monitoring systems. Their vigilance is likely because, as Kim says, “the penalties for the operator can be severe. It might be a fine. It might be the license getting pulled.”

Kalshi imposes similar prohibitions on its sports-related markets, using the same IC360 platform that’s used by betting platforms like Caesars Sportsbook. Kim says he doesn’t believe this type of monitoring is something the CFTC explicitly requires of prediction markets. Cristea agreed that it may not be specifically mandated, but noted that CFTC-regulated prediction platforms must demonstrate they can effectively police their markets against manipulation. For Kalshi, implementing monitoring systems like IC360 likely helps prove to the CFTC they’re upholding their licensing obligations.

While Kalshi imposes strict trading restrictions on its presidential election market — barring politicians, campaign staff, pollsters, election officials, and foreign nationals — many of its other markets lack any such prohibitions. This includes election-related markets identical to the type of bet Ackman suggested Adams could place on Polymarket about his own mayoral campaign withdrawal.

Polymarket, which does not yet serve US customers, does no such screening. The platform merely asks users to self-certify they aren’t US-based, with additional basic geofencing that users regularly circumvent. Polymarket doesn’t require any additional identity verification, and its cryptocurrency-based trading allows users to remain largely anonymous. It remains to be seen whether, and how, the platform will implement more rigorous screening as it looks to re-enter the US — potentially alienating a crypto-native user base often resistant to identity verification requirements.

With markets on such a wide range of events, these platforms can intersect with multiple regulatory frameworks: gambling law, securities regulations, and election integrity rules. Election markets in particular have sparked intense debate, with the CFTC initially opposing them outright. When moving to prohibit Kalshi’s Congress-related markets, then-Chairman Rostin Behnam argued they would force the agency to become an “election cop”. This would mean “monitoring elections, candidates, and countless participants in the political machinations that proliferate in the media and cyberspace in an effort to prevent manipulation and false reporting within the political system” — a role Behnam said the CFTC “currently lacks the mandate to do.”6 But after losing its court battle with Kalshi, the agency had little choice but to allow these markets, and Kalshi has since dramatically expanded its election-related offerings.

The stakes of prediction markets

Platforms like Polymarket and Kalshi have already grown far beyond niche experiments, sometimes reporting over a billion dollars in monthly trading volume with hundreds of thousands of active traders. Regulators and lawmakers now face questions: Should these platforms face the same oversight as gambling operations? What obligations do they have to protect vulnerable users from addiction and financial harm? And can CFTC oversight alone prevent market manipulation and other misconduct?

The gambling question has become particularly contentious when it comes to sports markets, which dominate trading activity on prediction platforms like Kalshi.7 State regulators have argued these offerings violate state-level gambling laws, with Massachusetts being the most recent to file a lawsuit against Kalshi on September 12. In a statement, Attorney General Andrea Joy Campbell stressed, “sports wagering comes with significant risk of addiction and financial loss and must be strictly regulated to mitigate public health consequences.”8

State gambling laws vary but typically require operators to pay special taxes, implement rigorous age and location verification, and establish addiction prevention programs. While Kalshi prohibits users under 18, this falls short of some state requirements — Massachusetts, for instance, sets the minimum age for sports betting at 21. And though Kalshi offers voluntary self-exclusion for problem gamblers, they lack the automated safeguards required by some states, such as notifications or even forced cooling-off periods when users show signs of addictive behavior like rapid deposits or erratic bets.

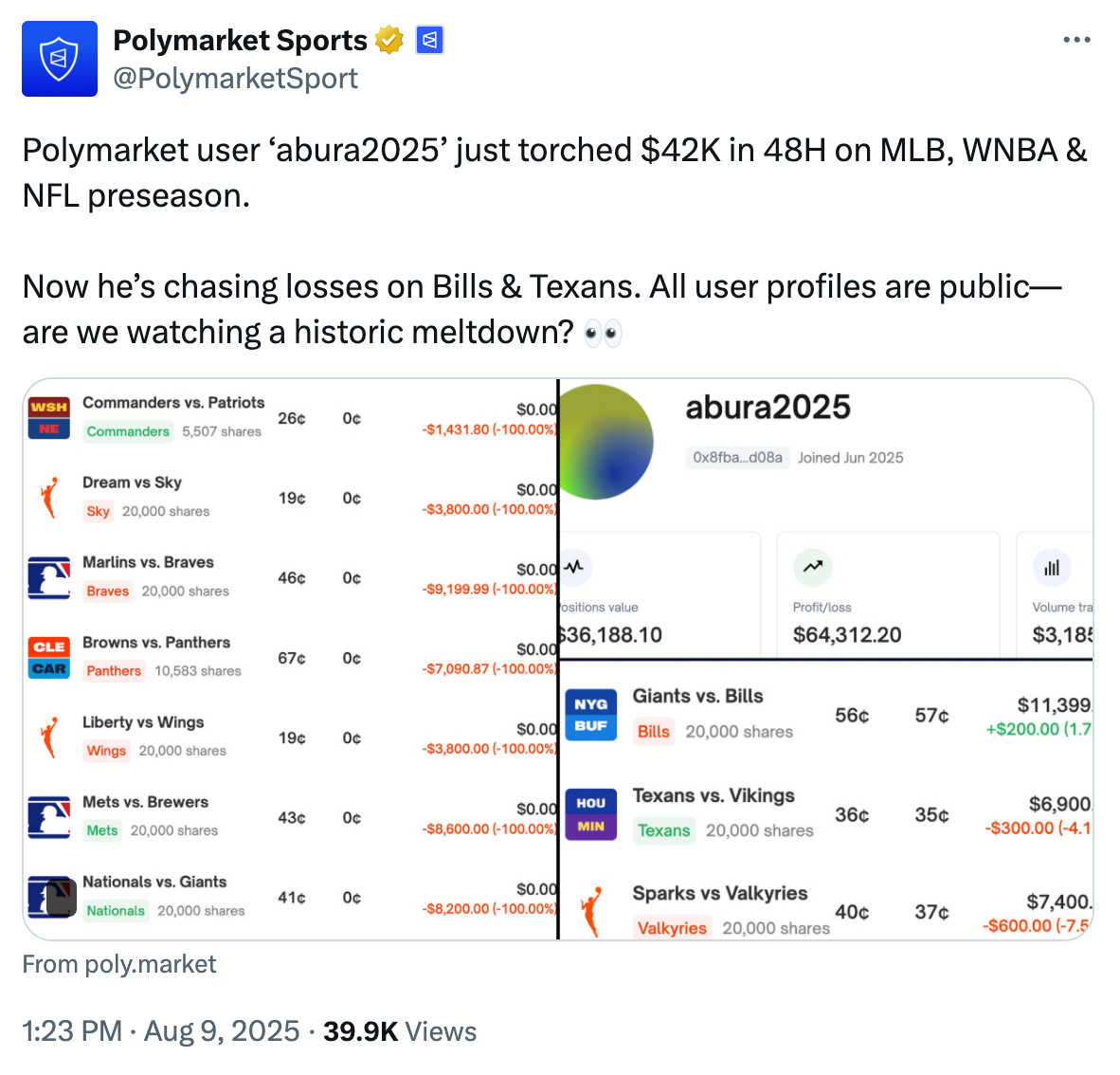

Platforms like Polymarket have even fewer restrictions. Without identity verification requirements, anyone with access to cryptocurrency can trade, including minors. The platform lacks even basic voluntary self-exclusion options, let alone more proactive safeguards. And problem gambling experts have called out the platform’s troubling attitude toward addiction.9 In one incident, an official Polymarket Twitter account highlighted a trader who had lost more than $40,000 on sports bets over two days, and publicly ridiculed them: “Now he’s chasing losses on Bills & Texans. ... Are we watching a historic meltdown?”

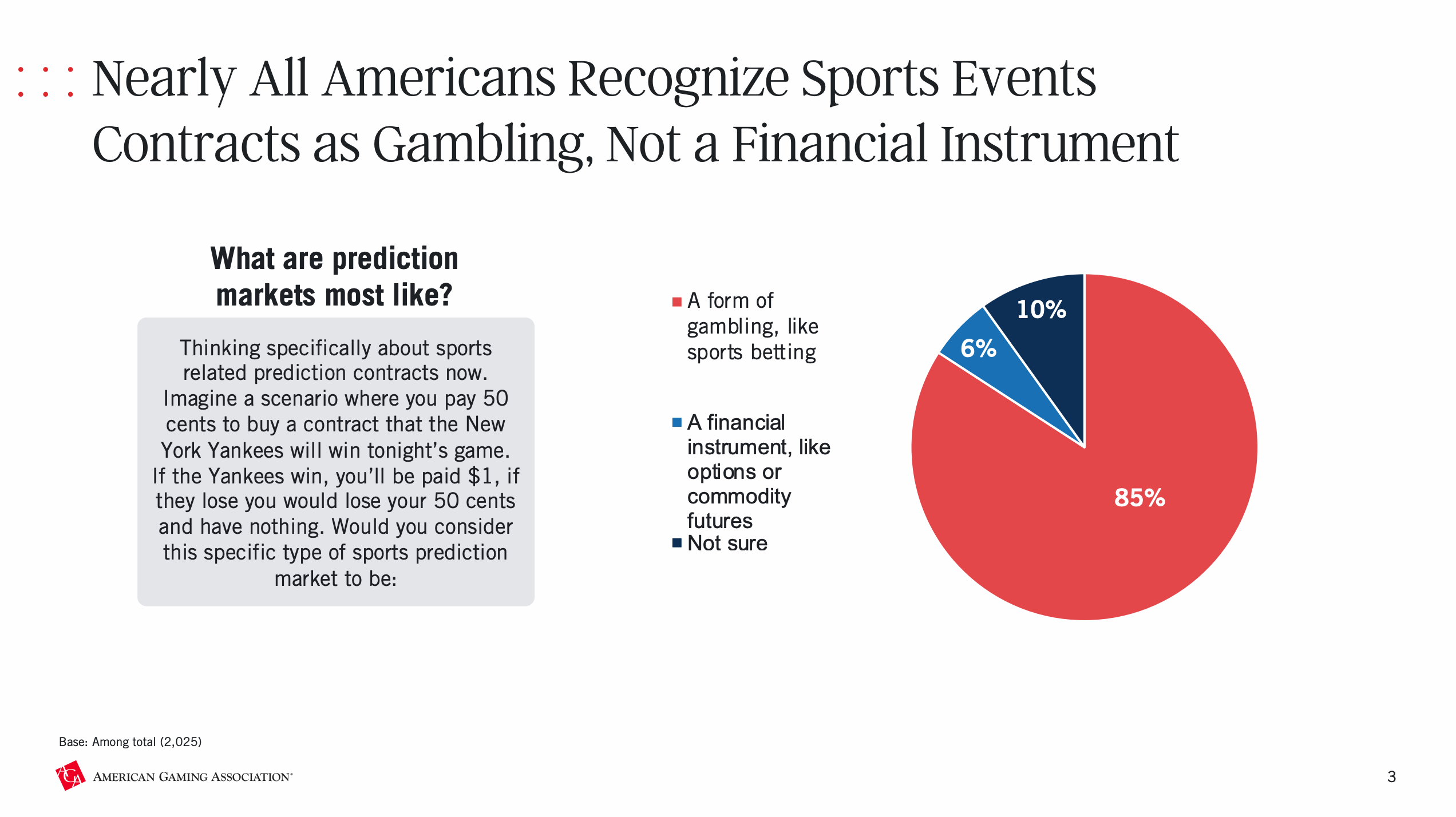

These platforms maintain that they offer financial services that shouldn’t be considered wagers. But are they really so different? “Pragmatically, I think for the retail individual, they don’t see a difference,” says Kim. “I think retail individuals trading on these platforms are not thinking of it as not gambling. They’re just thinking of it as one more outlet for them to participate in the opportunity to put money on an event.” Recent research supports this, with a study from the American Gaming Association finding that most Americans view sports-related prediction markets as a form of gambling.10 But at the same time, Kim sees some legitimate arguments from these platforms that they are offering swaps and not wagers, at least when it comes to a strict reading of the law.

I posed the same question to Cristea. “What’s the difference between gambling and trading? The difference is likely whether certain activity is done on a federally-regulated market, like a CFTC or SEC registered exchange.” He acknowledged that, particularly for unsophisticated investors, the line between gambling and trading can be blurry regardless of where they’re placing their bets or trades. “If you have a gambling addiction, could you satisfy it by going and trading an oil future or a gas contract or a Microsoft stock? Maybe. ... I mean, there are people who are day trading, right? And if you talk to anybody about day trading, especially people who work in finance, they will likely say, ‘oh no, I invest in ETFs, money market or mutual funds. Day trading is like gambling all the way.’”

When Kalshi self-certifies each contract to the CFTC, it attests that these markets serve a legitimate economic purpose, such as hedging, price discovery, or risk management. But many of its offerings have no plausible connection to those functions. Sure, there are probably more sports fans recreationally placing trades on who’s going to make it to the later rounds of March Madness, but one could argue that a bar operator might theoretically use these markets to hedge against uncertain revenue if their local team fails to advance. But this kind of rationale is harder to find across many of Kalshi’s other contracts, such as who will serve as a bridesmaid at the wedding of Travis Kelce and Taylor Swift, or whether a popular YouTuber will cut his hair on stream. Polymarket, which does not yet answer to the CFTC, has even more egregious examples: Will Hailey Bieber get pregnant this year? Will the Obamas divorce? Will Trump say the word “pizza” in September? These markets seem far removed from the original purpose of futures trading — under the Commodity Exchange Act, the justification for letting futures markets exist outside gambling law has always been that they serve an economic function by giving commercial actors tools to manage risk.

Election integrity presents another major concern, as prediction markets create new financial incentives that some fear could (further) distort democratic processes. When defending its ban on Kalshi’s Congressional contracts in court, the CFTC found support from consumer rights advocacy groups like Public Citizen, whose Lisa Gilbert warned that “layering in gambling on our elections will take our democracy in precisely the wrong direction.”11 In an amicus brief, the financial reform group Better Markets argued these markets threaten both investors and democratic institutions.12 “Evidence is fast emerging that these types of election wagering contracts may already be serving as instrumentalities of either election manipulation for political gain, market manipulation for financial gain, or both,” they wrote, citing a Wall Street Journal article suggesting that Polymarket traders might have been artificially pumping up contract prices on a Trump election victory.13

Going back to Ackman’s idea: directly paying a candidate to drop out of a race is likely illegal, but it’s not clear if laws aimed at maintaining election integrity could be applied to prediction markets. Public Citizen’s government ethics expert Craig Holman is skeptical. “I do not see how that type of unethical election gambling would be illegal, even if you could prove deceptive intent,” he explains.

Finally, there’s the question of whether the CFTC is equipped to handle these surging markets, and the demographic they attract. Unlike state gambling commissions, the CFTC’s primary focus is on fraud and market integrity, not addiction or financial harm to amateur traders. Will it need to expand its mandate to address these consumer protection issues, or will some other regulator need to step in? Cristea says there isn’t a clear right answer. “Maybe there does need to be some sort of retail protection in there.”

Stark offers a different possibility: “I just don’t know if anyone cares if the Polymarket marketplace is completely corrupt — that is the sole reason to police that sort of conduct. If uninformed participants don’t care that betting in Polymarket becomes like betting on a World Wrestling championship match outcome, then regulators won’t care either.”

Unanswered questions

When Bill Ackman casually suggested Eric Adams could “fund his future” by betting on his own withdrawal from the mayoral race, he inadvertently highlighted some of the thorny questions around prediction markets. The industry’s growth under Trump’s deregulatory agenda is likely just beginning, and more companies are entering the space — from crypto exchanges to gambling platforms. Some will probably follow Kalshi’s playbook of aggressive litigation to expand the range of permissible contracts. Others may copy Polymarket’s approach of trying to skirt regulatory authority with crypto-denominated trades. Some gambling platforms may attempt a version of regulatory arbitrage, particularly if the outcomes of ongoing court cases suggest that such companies can dodge heavy taxes and onerous compliance burdens by reinventing themselves as trading platforms.

Without much oversight, these markets are ripe for manipulation. The gambling-like nature of many markets, combined with limited addiction prevention programs, likely puts vulnerable users at risk. And election markets create concerning new financial incentives that could further corrupt democratic processes.

Can the CFTC, traditionally focused on institutional traders and commercial hedgers, effectively oversee retail-heavy prediction markets? Should these platforms face the same strict integrity requirements as sportsbooks, barring insiders from trading on events they can influence? Should betting on political outcomes be allowed, or will it inevitably create perverse incentives that could undermine democracy? What types of events should be eligible for trading? Weather events and inflation rates might seem relatively uncontroversial, but what about contracts that could incentivize harmful real-world actions? And how should regulators balance consumer protection against personal responsibility when it comes to retail traders who may be, essentially, gambling beyond their means?

With prediction markets already handling billions of dollars in trades and more platforms launching every month, regulators need to grapple with these questions before the industry grows too big to effectively control. The cryptocurrency industry has shown how difficult it becomes to implement meaningful oversight once a poorly regulated industry accumulates enough money and political influence to push back — and the devastating cost to everyday people who get caught in the fallout.

Have information? Send tips (no PR) to molly0xfff.07 on Signal or molly@mollywhite.net (PGP).

I have disclosures for my work and writing pertaining to cryptocurrencies.

Footnotes

With the caveat that the SEC could theoretically bring a case if they decided these markets were influencing securities markets. ↩

References

“CFTC Orders Event-Based Binary Options Markets Operator to Pay $1.4 Million Penalty”, CFTC. ↩

“CFTC Staff Withdraws No-Action Letter to Victoria University of Wellington, New Zealand Regarding a Not-For-Profit Market for Certain Event Contracts”, CFTC. ↩

Motion for summary judgment filed on January 25, 2024. Document #17 in KalshiEx LLC v. CFTC. ↩

“Statement of Chairman Rostin Behnam Regarding CFTC Order to Prohibit Kalshi Political Control Derivatives Contracts”, CFTC. ↩

“Kalshi Trading Volume Soars As Football Betting Season Kicks Off”, LegalSportsReport. ↩

“AG Campbell Sues Online Prediction Market for Illegal and Unsafe Sports Wagering Operations”, Office of the Attorney General for Massachusetts. ↩

“Polymarket Publicly Shames Person Showing Signs Of Problem Gambling”, Gambling Harm. ↩

“Sports Event Contracts: Public Opinion Landscape”, American Gaming Association. ↩

“CFTC Must Reject Dangerous Election Gambling Proposal”, Public Citizen. ↩

Amicus brief by Better Markets, filed on October 23, 2024. Document #2081637 in KalshiEx LLC v. CFTC. ↩

“A Mystery $30 Million Wave of Pro-Trump Bets Has Moved a Popular Prediction Market”, The Wall Street Journal. ↩