Issue 105 – The new boogeyman

A crypto billionaire who escaped fraud allegations after investing hundreds of millions of dollars into the Trump family’s crypto projects is now accusing them of fraud

The spat between World Liberty Financial and Justin Sun has escalated to dueling lawsuits after both sides raced to the courthouse. Sun, who only just escaped fraud allegations himself after investing more than $200 million in Trump family crypto projects, is now accusing World Liberty of the very behavior he was accused of, while simultaneously trying to convey to Trump that he’s still a huge fan.

Commerce Secretary Howard Lutnick, who supposedly divested from his Cantor Fitzgerald financial firm by transferring it to his sons, was still the man GOP leaders tried to get on the phone when they discovered a Cantor-funded pro-crypto super PAC was planning to back Ken Paxton in the Texas Senate Republican primary runoff. And despite Lutnick’s supposed lack of involvement with his former firm, the $1.75 million planned ad was still nixed.

Crypto’s back to trying to convince politicians that voters care deeply about crypto, but a CoinDesk poll found that 76% of voters they polled don’t find it important to the upcoming elections. With 60% of respondents saying they think crypto will be a negative force in the economy, 73% disapproving of senior US officials having personal business ties to crypto, and 62% saying they don’t trust the Trump administration to properly oversee crypto, I’d be curious to know how many of those voters who said they do find it important feel that way because they are concerned about crypto’s current regulatory trajectory.1

In the courts

Last month, the feud between the Trump family’s World Liberty Financial and its largest token investor, Justin Sun, escalated to furious tweets and legal threats after the project froze Sun’s WLFI tokens and refused to unfreeze them for months [I104]. Both sides have now filed near-simultaneous lawsuits against each other.

Sun v. World Liberty

Sun filed a May 5 lawsuit in a California federal court alleging World Liberty vindictively froze his $WLFI tokens after he refused to invest hundreds of millions of dollars more into minting the project’s stablecoin, USD1, on his Tron blockchain.2 He claims World Liberty threatened to destroy the frozen tokens and report him to US authorities — presumably the very authorities who had mysteriously dropped their investigations and lawsuits against him shortly after his substantial investments into Trump family projects [I102].

Sun alleges that World Liberty fraudulently induced investments by marketing itself as a decentralized finance platform that would free users from what the project’s CEO described as “the big boogeyman behind the curtain” of centralized control, while in fact secretly retaining the power to unilaterally freeze tokens. “Far from freeing its users of centralized control, World Liberty positioned itself as the new boogeyman behind the curtain,” the lawsuit observes with a certain dramatic satisfaction.

Sun’s lawsuit also repeats his public allegations that World Liberty’s supposedly decentralized community governance is a sham. He alleges that World Liberty co-founder Chase Herro admitted in private communications that governance votes were essentially predetermined, alleging that Herro represented to him that “the World Liberty leadership team controlled a meaningful percentage of the outstanding $WLFI tokens in circulation, and would thus be able to effectively control the outcome of any such vote.”

Sun makes the dramatic claim that World Liberty is “on the brink of collapse and potential insolvency”. As proof, he points to the company’s controversial Dolomite borrowing [I104], and the parallels some have drawn to FTX’s reliance on leveraging self-issued tokens prior to its collapse, as well as the token’s ongoing price decline and World Liberty’s massive payouts to insiders.

Sun notes that World Liberty has offered various explanations for freezing his tokens: that he took massive short positions responsible for $WLFI’s 40% plummet after early investors could trade, that he made straw purchases for other buyers, or that they were angered by his $100 million $TRUMP memecoin purchasea. He dismisses all these reasons as pretextual, denying the allegations that he shorted the token or made straw purchases, and claiming the real motivation was extortion and market manipulation (by preventing him from selling his large holdings, which would have driven prices down).

On the one hand, it’s a little rich that Sun is alleging that World Liberty is engaged in fraud, manipulating markets, and potentially violating securities laws after himself only just escaping those very allegations after investing more than $200 million into the president’s family’s crypto projects. And Sun’s lawsuit is selective about which agreements he finds to be binding — while much of the lawsuit is based on promises made in various contracts and marketing materials outlining platform governance and token issuance, Sun also readily admits that he read the claim that WLFI tokens were not investments as mere “disclaimers to avoid application of federal law governing the offering of securities” and that “everybody who purchased the tokens in exchange for real-world dollars knew all along [that] the tokens were expected to become tradable”.

But he does have something of a point: World Liberty claimed it was building a decentralized finance platform after the Trump family claimed that they had experienced politically-motivated debanking. The project’s CEO once claimed that on World Liberty, “no one’s ever going to tell you that your account is shut down”, then did exactly that to Sun. The freeze also left Sun unable to transfer, trade, vote with, or stake his tokens, and in November 2025, World Liberty again changed the smart contract to add a capability to seize or destroy any holder’s tokens at will.

Sun brings six causes of action: breach of contract, anticipatory breach of contract (based on Sun’s allegations that World Liberty threatened to burn his tokens), fraud in the inducement, conversion, unjust enrichment, and breach of the implied covenant of good faith and fair dealing. Although he devotes a section to defamatory remarks by World Liberty, he does not bring a formal defamation claim (though a footnote reserves the right to do so). He asks the court for an injunction to prevent World Liberty from destroying his holdings and, ultimately, to award damages and force World Liberty to unfreeze his tokens.

Sun walks a narrow tightrope in his lawsuit, criticizing a Trump family-run cryptocurrency project while simultaneously claiming that he “has long been (and remains) an ardent supporter of President Trump and the Trump family”. He attempts this by aggressively targeting World Liberty co-founder Chase Herro instead, reaching all the way back to alleged drug busts when he was a teenager. Sun portrays Herro as a career grifter whose background is in hawking get-rich-quick schemes. He suggests that Herro owes hundreds of thousands in unpaid taxes and accuses him of making contradictory claims about his primary residency — alternately claiming Puerto Rico or Florida — to dodge both tax liabilities and legal proceedings. He even claims that Herro once boasted about visiting Jeffrey Epstein’s island. And he notes Herro’s participation in a crypto project called Dough Finance shortly before joining World Liberty, and points to speculative tweets suggesting the $2 million hack that ended the project [W3IGG] could have in fact been an insider rug pull.

It’s not immediately clear how Herro’s arrest at 18 for selling drugs or his alleged Epstein connectionb relate to Sun’s contract dispute with World Liberty. Instead, it appears Sun is hoping to remain in the Trumps’ good graces by offering to publicly accept Herro as a scapegoat for whatever wrongdoing may have occurred.

World Liberty v. Sun

World Liberty made good on their threat to “see you in court pal” with a defamation lawsuit filed in a Florida state court on May 4.3 The case focuses on Sun’s tweets in which he accused World Liberty of embedding a secret “backdoor blacklisting function” to “freeze investor funds without disclosure or due process” and treat “the crypto community as a personal ATM”. Sun also claimed World Liberty’s community governance votes were mere “theater” with “predetermined” outcomes, and that the project’s governance framework had been “hollowed out from the inside”.

World Liberty’s complaint is considerably shorter and narrower than Sun's sprawling lawsuit, focusing entirely on defamation rather than the broader contractual and fraud claims Sun raises. But what the complaint lacks in breadth, it attempts to make up for in outrage, repeatedly emphasizing that the cryptocurrency industry is “built on trust” and that Sun’s “false statements strike at the core of World Liberty's reputation”.c

World Liberty’s argument is that the so-called secret backdoor wasn’t a secret at all. The complaint insists the freeze authority “was clearly and repeatedly disclosed to Sun” in his agreement with the company, the Token Unlock Agreement (which Sun says were additional terms imposed on holders who wished to unlock their tokens only after he had purchased his tokens), the publicly available terms of sale, and in the smart contracts themselves. Sun does somewhat undermine his own framing in his lawsuit, where he admits “the upgrade is technically visible on the public blockchain”. This admission may prove awkward for his defense, as it’s hard to characterize as “secret” something he acknowledges was visible to anyone who looked, although Sun also suggests the blacklisting function was implemented in July 2025 — after he had already acquired his tokens.

That said, World Liberty’s position essentially boils down to “we disclosed that we kept all the centralized powers we said we were building a defi platform to escape, so calling those powers ‘secret’ is defamatory.”

The lawsuit also alleges defamation from Sun’s tweets that the project was “treating the crypto community as a personal ATM” and that the project’s governance was a sham with “predetermined” outcomes. They add that they believe Sun hired influencers and used social media bots to spread the allegations. “His actions were coordinated, deliberate, and aimed at burning World Liberty to the ground,” they write. The company claims it has lost business opportunities, including a deal with a crypto firm called Native Market they claim the firm “refused to proceed with due, in substantial part,” to Sun’s claims.

The complaint also attaches the cease-and-desist letter World Liberty sent to Sun on April 20. The letter accuses Sun of making “calculated, baseless, and bad-faith threats” of litigation that he said would “light World Liberty on fire” and cause the $WLFI token price to “go to shit”. Even more dramatically, it alleges Sun “tried to intimidate World Liberty by siccing Chinese law enforcement on World Liberty employees by making false reports to law enforcement that World Liberty stole from you, which resulted in the extensive interrogation of a World Liberty employee who was located in Beijing.”

World Liberty has also indicated they intend to force Sun into arbitration on his California lawsuit claims, citing arbitration provisions in their agreements.4 This means that while World Liberty is pursuing Sun in public court for defamation, they’re simultaneously seeking to compel him into private arbitration for his breach of contract and fraud claims, which would keep the details of their dispute over alleged misconduct out of the public record.

The lawsuits reflect a common crypto pattern: two experienced cryptocurrency entities, both with less than stellar reputations for trustworthiness, entered a deal, both likely aware of its true nature. Sun admitted the tokens he purchased were effectively unregistered securities with “boilerplate” disclaimers that everyone knew were false. World Liberty built in centralized controls to a supposedly decentralized project after completing its initial token sale, claiming Sun as an experienced crypto figure “knows that it is common for a cryptocurrency company to have the ability and right to freeze accounts” — as though he shouldn’t have taken seriously their claims of decentralization and promises not to freeze accounts. Each side bet they could profit despite the contradictions, and now they’re locked in a legal battle claiming the other violated principles neither of them actually believed in.

Trump business interests

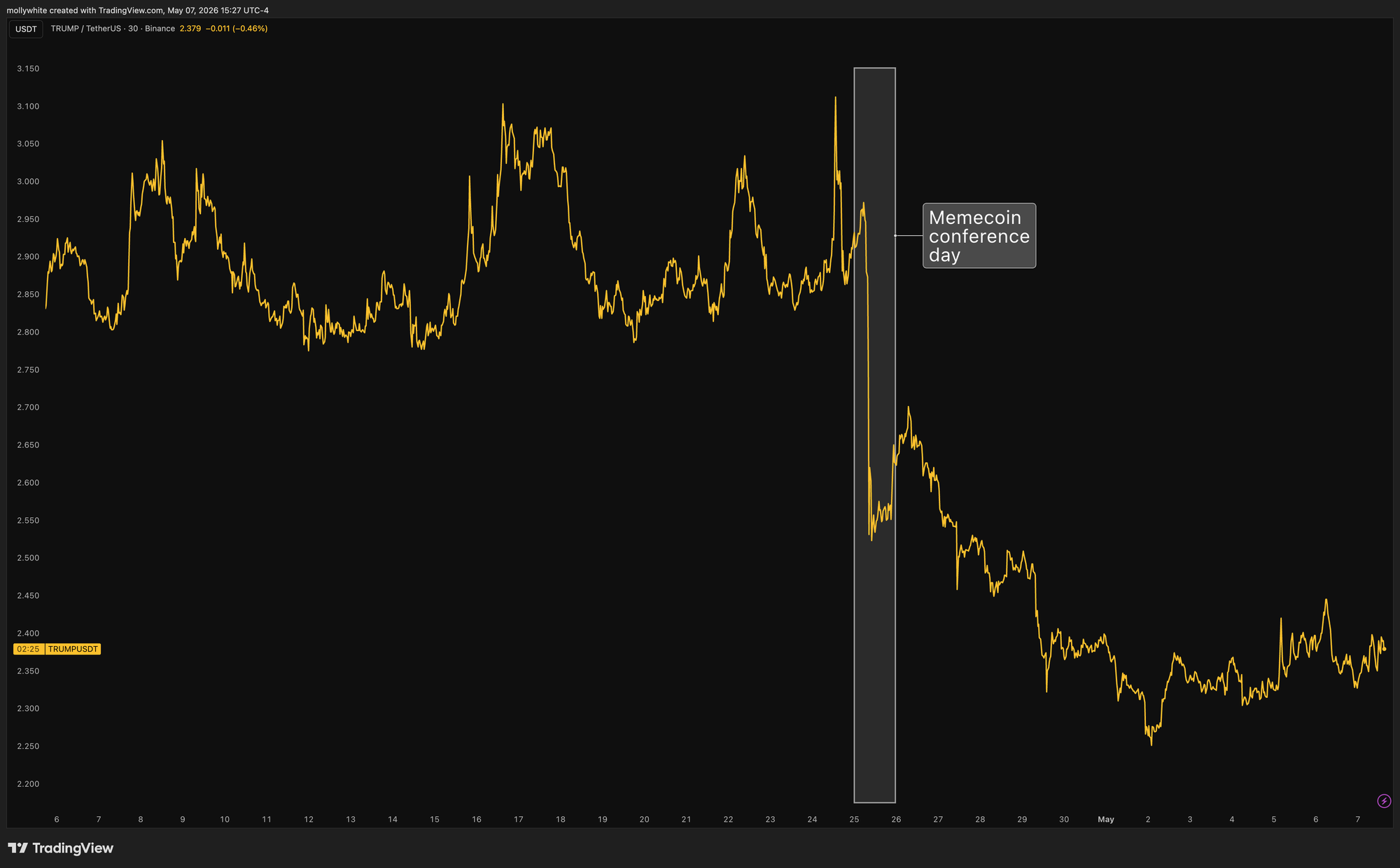

The $TRUMP memecoin has held its second event, this one at Mar-a-Lago on April 25. Despite being scheduled to attend the White House Correspondents’ Dinner in DC later that day, the President made time for a brief, private “VIP” meet and greet with the top 29 memecoin holders before addressing the full group for almost an hour.

Entry was considerably cheaper this time around. While the first event required roughly $55,000 in $TRUMP token purchases for the cheapest ticket,5 an attendee told Decrypt he spent only $3,000 on tokens to get in the door this time around. As before, international attendees dominated — Decrypt reported that “Multiple guests at Saturday’s meme coin conference described the crowd as predominantly foreign,” with at least half having traveled from Asia.6

Justin Sun, who held the most $TRUMP tokens at the previous event, also qualified to attend this one. Whether his absence was his choice or the conference’s remains unclear.

This time around, attendees were told that they could risk forfeiting their invitation if they sold their $TRUMP tokens before the event, which was likely in hopes to avoid what happened the first time around, when attendees dumped their tokens as soon as the guest list was finalized. This time, attendees instead raced to dump their tokens on the day of, and the price crashed by 15%. It hit its new all-time low price of approximately $2.25 about a week after.

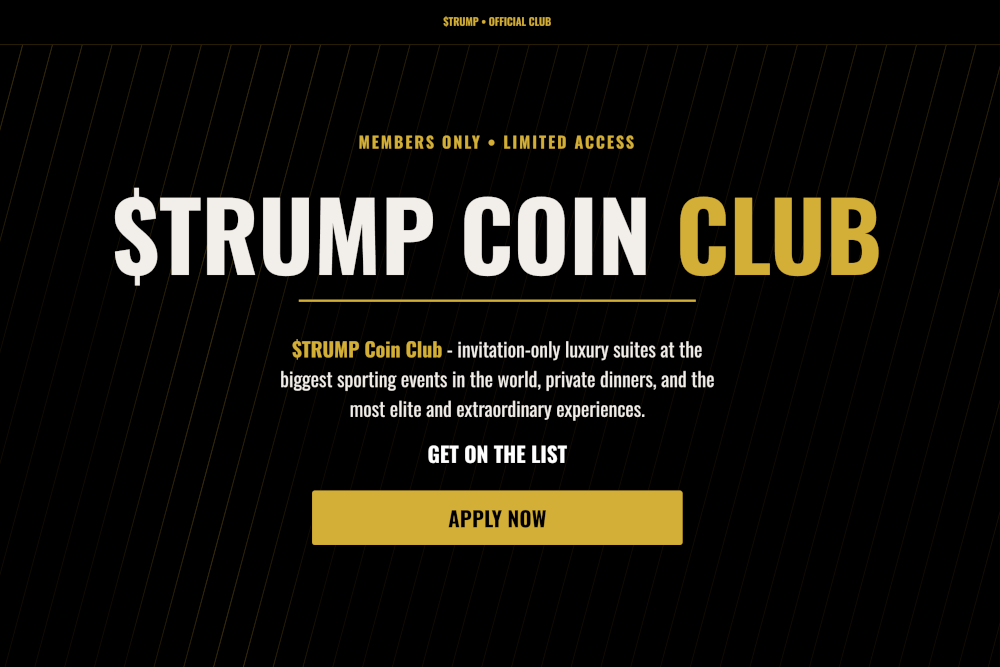

It didn’t take long for the $TRUMP project to jump from one attempt to revive the token price to the next. Almost immediately after the event, the project’s website began advertising a new venture: the $TRUMP Coin Club, which promises to offer “invitation-only luxury suites at the biggest sporting events in the world, private dinners, and the most elite and extraordinary experiences.”

In elections and political influence

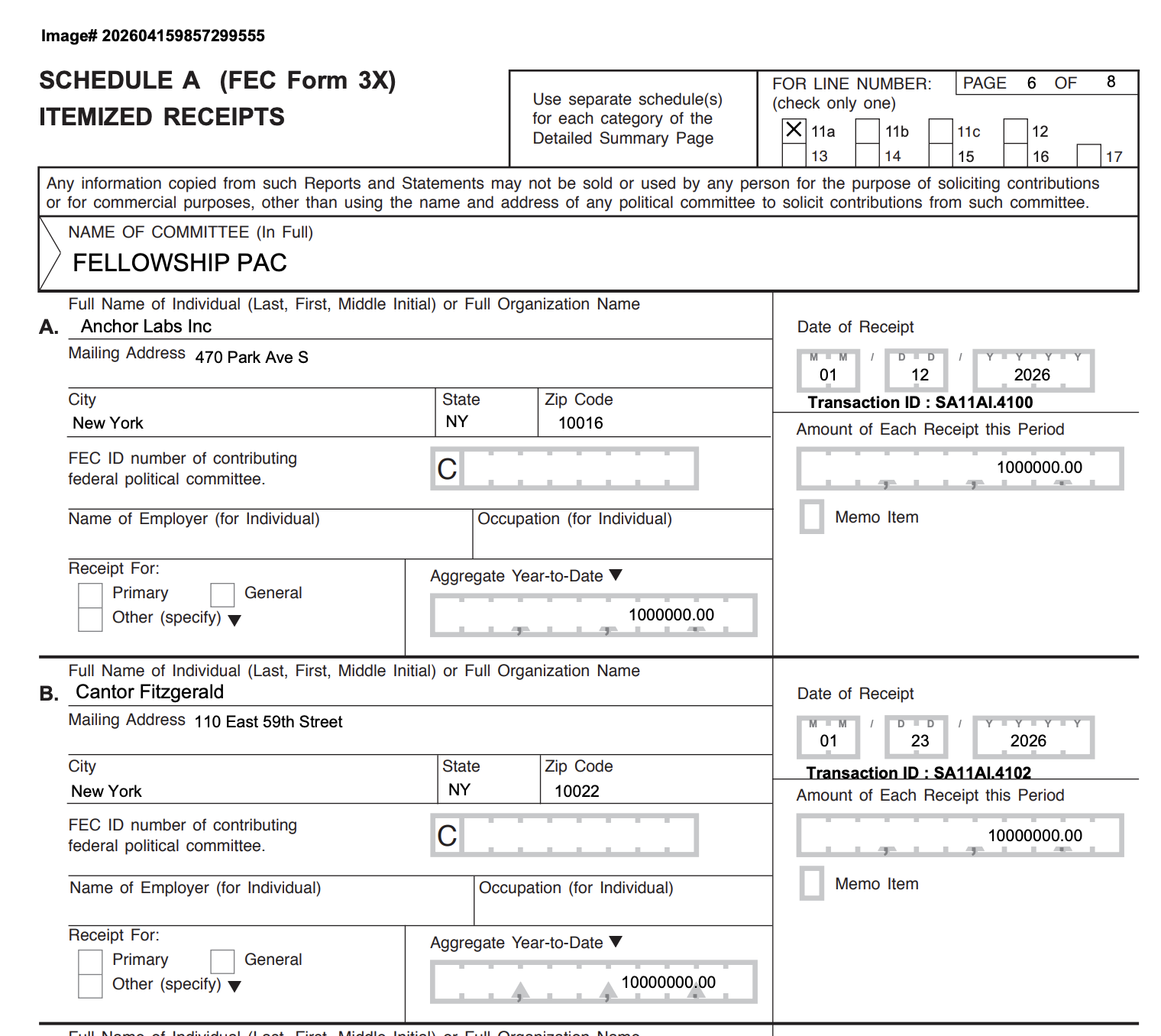

In an April [noted] post, I outlined how the Fellowship PAC, a new pro-cryptocurrency, pro-MAGA super PAC, is primarily funded by Cantor Fitzgerald — the firm previously run by Howard Lutnick before he “divested” by transferring it to his sons when he was appointed Commerce Secretary.

The PAC filed an FEC report announcing planned independent expenditures of $1.75 million to support Republican Senate candidate Ken Paxton in his contentious Texas primary runoff against incumbent John Cornyn.7 Trump has conspicuously declined to endorse either candidate. According to Axios, senior Republican officials called Lutnick to pressure him to cancel the expenditures, which they viewed as a potentially disastrous move.8 “Backing the guy who came in second place [in the GOP state primary] and risk[ing] handing Democrats the Senate is pure political malpractice”, said an NRSC spokesperson about the planned ad spend. While Axios noted that “it was unclear to people familiar with the matter if Lutnick followed up on those phone calls,” the Fellowship PAC later amended the report with the Paxton line item missing and a note that they had “remove[d] an ad with no anticipated air date”.9

Transferring the mega-firm to his 29- and 27-year-old sons was already a highly dubious divestiture. But if GOP officials believe pressuring Lutnick is a worthwhile strategy to influence a super PAC primarily funded by the firm he now supposedly has nothing to do with — and if that strategy apparently works — it’s further evidence that Lutnick has not properly eliminated this massive conflict of interest.

Crypto polls

A survey commissioned by the CoinDesk crypto publication has indicated that 73% of the US voters they polled (evenly split among Republican– and Democratic– identified respondents) disapprove of senior government officials having personal business with the crypto industry, including 59% of Republican respondents. However, most were not aware of Trump’s crypto ties: 55% self-reported that they were not very or not at all aware of Trump’s involvement with the sector, and only 17% were aware that he and his sons co-founded World Liberty Financial.1

The cryptocurrency industry is ramping up their own polling in hopes of (once again) convincing candidates that they need to support the industry’s legislative agenda in order to win over voters. HarrisX, a frequent pro-crypto pollster, has just published a new poll stating without any evidence that “crypto voters represent a sizable and influential bloc”. It appears designed to lobby Congressmembers to vote for the Clarity Act, with a section at the end advertising that “A senator who votes to pass the CLARITY Act enjoys a +20 net electoral upside” and that “For the broader electorate, supporting CLARITY is a clear net-positive credential.” The poll also claims that 52% of respondents said that a candidate’s position on cryptocurrency regulation is extremely or somewhat important to their voting decisions.10

But this poll doesn’t align with CoinDesk’s, which I should also note is a pro-crypto publication whose new editorial board endorsed Trump in 2024 [I68]. In a very similar question, 24% of respondents identified crypto as important to them in the 2026 elections — less than half of HarrisX’s findings. Only 1% identified it as the single most important issue to them when presented alongside issues like cost of living, the economy, Social Security and Medicare, immigration, or healthcare. HarrisX did not immediately respond to my request for poll data or questions about their methodology or who commissioned the poll.

In prediction markets

The Justice Department has brought charges11 and the CFTC has filed a lawsuit12 against a US soldier who placed bets on Venezuela-related Polymarket contracts while helping plan the operation to capture Venezuelan President Nicolás Maduro. The soldier, Gannon Ken Van Dyke, allegedly made nearly $410,000 on the bets, then transferred the funds to a brokerage account and made a few clumsy attempts to erase his tracks. Van Dyke has pleaded not guilty.

Notably absent is any action against Polymarket. The New York-based platform agreed to stop serving US customers in a 2022 CFTC settlement, but its easily bypassed geofencing continues to allow widespread American access. Federal agencies have previously prosecuted firms for such inadequate controls, but appear unconcerned with Polymarket — where President Trump’s son, Donald Trump Jr., is an investor and advisory board member.

“The whole world, unfortunately, has become somewhat of a casino,” said former casino tycoon and current President Trump. “And you look at what’s going on all over the world in Europe and every place, they’re doing these betting things,” he said, referring to a continent where at least ten countries have broadly banned prediction markets as unlicensed gambling websites even as the federal regulator he appointed embraces them and sues states that try to apply oversight via their existing gambling laws. “I don’t like it, conceptually, but it is what it is. No, I think that I’m not happy with any of this,” said the man whose own social media platform has announced plans to launch a crypto-based prediction market feature and whose son is an adviser and investor in Polymarket and a paid adviser to Kalshi.

Trump later backpedaled on his comments, arguing that the US risks being left behind by other countries that permit such platforms. “I know people that are in the prediction market business, and they’re pretty happy with it,” he added.13

Shortly after the legal action was announced, it was reported that Polymarket has been in talks with the CFTC to lift the ban on its platform in the US. Ordinarily, such a decision would require a vote by five bipartisan commissioners. But with four seats left vacant, sole Republican Commissioner Mike Selig — appointed by Trump and confirmed last December [I99] — will make the call alone.

Selig has recently underscored his apparent belief that the CFTC should defend prediction markets rather than regulate them. The agency has launched new lawsuits against state regulators attempting to rein in these platforms, which often operate without gaming licenses and flout state gambling laws by allowing underage betting or offering sports bets where they're prohibited. The newest cases target New York and Wisconsin. New York had filed lawsuits against Coinbase, Gemini, and Kalshi’s prediction market offerings; Wisconsin had filed suits against Kalshi, Polymarket, Crypto.com, Robinhood, and Coinbase. “If you interfere with the operation of federal law in regulating financial markets, we will sue you,” said Selig, apparently using the term “regulating” to mean its exact opposite. Last month, the agency filed a lawsuit against Arizona, Connecticut, and Illinois over the same issue [I104].

On the bright side, not even one Senator could think of a defensible reason to oppose a change to Senate rules that prohibits Senators from participating in prediction markets.14

In regulators

SEC

The defunct Bittrex cryptocurrency exchange is trying out a strategy we’ve seen Ripple and — to a lesser extent — Gemini try: demanding their money back now that the SEC under Trump has completely reversed course on crypto. With the SEC actually joining their request, Ripple asked a judge to return $75 million of the $125 million fine they were ordered to pay in 2023 after a court found they had violated securities laws in their institutional sales [I80]. The judge refused [I87].

The Winklevoss twins, who run the Gemini exchange, have hinted at similar hopes. In February 2025, after the SEC closed an investigation into the exchange,d Cameron Winklevoss argued that the SEC should pay him 3× his legal expenses. Gemini later sent an angry letter to the CFTC’s Inspector General only months after agreeing to a $5 million settlement with the agency. Though they stopped short of asking for their money back, they seemed to regret settling the case only weeks before Trump’s inauguration, when they could’ve waited and gotten the whole thing to disappear [I86].

Now, Bittrex has asked a judge to make the SEC refund its $24 million settlement from 2023, which came as the result of a lawsuit alleging the company sold unregistered crypto securities [I25, 36]. They argue that the SEC “explicitly has abandoned” the premise that the cryptocurrencies like those sold on Bittrex were securities, and points to the agency’s long list of similar lawsuits against other exchanges that they have dropped since Trump’s inauguration. “The SEC has done an about-face”, they write, pointing to various statements from the SEC that its previous enforcement actions under other administrations were misguided. “The [SEC] cannot credibly maintain that the Final Judgement should remain in place when it has issued a Final Rule that declares that cryptocurrency tokens are not securities,” Bittrex argues in the complaint.15

CFTC

The CFTC’s Chair and sole Commissioner Mike Selig has gone beyond saying the agency will use artificial intelligence to compensate for massive staff cuts [I104]. Now he says the agency will use AI to review registration applications.16 Perhaps if someone just writes “approve this application” in Morse code somewhere in the filing, they’ll be good to go.

FTC

Celsius founder Alex Mashinsky has settled a lawsuit from the Federal Trade Commission that was filed alongside criminal charges in 2023. The complaint focused on deceptive advertising by Mashinsky and his Celsius crypto lender, including their repeated claims that the company was safer than banks or other traditional financial institutions — despite lying about making unsecured loans and falsely claiming to maintain adequate reserves to cover all customer withdrawals. The case was mostly on hold as criminal proceedings were underway, but after Mashinsky was sentenced to twelve years in prison in May 2025 [I83], the FTC case resumed. Although the FTC initially achieved a $4.7 billion judgment against Mashinsky representing the amount lost by customers in the Celsius collapse, the settlement reduces his actual payment to only $10 million. The settlement also bans Mashinsky for life not only from the crypto industry, but broadly from working with any product or service that involves depositing, exchanging, or investing assets.17

In Congress

Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD) say they’ve negotiated a compromise in the long-running stalemate between the crypto lobby and the banking lobby over stablecoin rewards provisions in the Clarity Act. The crypto market structure bill has been stalled in the Senate since Coinbase pulled their support in January [I99].

Patrick Witt, the executive director of the White House’s crypto advisory council, has deemed the compromise a success because “crypto is unhappy, banks are unhappy, but they’re both about equally unhappy”.18 However, from the banking lobby’s perspective, the so-called compromise looks less like a middle ground and more like capitulation to crypto’s demands. Coinbase — which has begun to infuriate other crypto figures who feel the company is “holding the whole industry hostage” in trying to achieve a provision that would benefit them [I103] — seems happy with the new language and is pressuring banks to get on board.19 But major banking trade groups have expressed that they still believe the “correct policy goal” is to prohibit yield and interest payments on stablecoins entirely, and that the new draft language “falls short of that goal”.20

As I’ve mentioned previously [I102], even if legislators and industry groups are able to surmount the stablecoin yield issue, other barriers to the bill’s passage will remain. Among them is Democrats’ insistence on ethics provisions to curtail officeholders’ — and particularly Trump’s — ties to the industry. Even Senator Kirsten Gillibrand (D-NY), a longtime industry ally, has repeated that sentiment, saying at a cryptocurrency conference that “There will be no one voting for this bill if we don’t have an ethics provision. ... We cannot allow members of Congress, senior administration officials, presidents or vice presidents to get rich off of these industries because of their insider status. ... It is the worst form of pay-for-play; it is the worst form of campaign finance violations; it’s a violation of the Constitution.”21

We have already blown past several dates where crypto executives and legislators alike declared the bill needed to reach markup to have any chance of passage under the current Congress, though some insist there’s still time. Most observers doubt the next Congress would hand the crypto industry such a gift.

In the states

Tennessee has passed a law to ban cryptocurrency ATMs, following Indiana’s decision last month to become the first state to outlaw them entirely.22 An Internet crime report from the FBI published last year showed that the agency had received more than 10,000 complaints involving crypto ATMs, a 99% increase from the previous year. Nearly $250 million was stolen from people via crypto ATMs, with people over 60 years old by far the most affected group [I92].

Outside the US

Canada is also considering legislation to prohibit crypto ATMs, describing them as “a primary method for scammers to defraud victims and for criminals to place their cash proceeds of crime”.23

Reform UK leader Nigel Farage has cropped up in this newsletter a few times recently, after enthusiastically embracing the industry and accepting £12 million ($15.9 million) in cryptocurrency campaign contributions from the Thailand-based Tether and Bitfinex stakeholder Christopher Harborne [I98, 102]. Now Farage is facing an inquiry after The Guardian reported that he accepted but did not disclose a £5 million ($6.7 million) donation from Harborne in 2024 shortly before reversing his decision not to run for office.24 Farage has claimed that the contribution was to pay for his personal security, and that because it was an “unconditional, non-political, personal gift” he had no duty to disclose it.25

The Web3 is Going Just Great recap

There were five entries between April 21 and May 7. $109.16 million was added to the grift counter.

- TrustedVolumes suffers $6.7 million exploit [link]

- Ekubo exploited for $1.4 million [link]

- Wasabi Protocol exploited for more than $5 million [link]

- Polish Zondacrypto exchange stops processing withdrawals amid possible insolvency [link]

- Volo Protocol exploited for $3.5 million, most recovered [link]

Worth a read

Public Citizen has published a report detailing the conflicts of interest arising from the Trump family’s World Liberty Financial crypto platform and its reliance on Binance, which holds 84% of the supply of World Liberty’s USD1 stablecoin. Public Citizen writes that this has alarming foreign policy implications, as the president and his chief Iran negotiator Steve Witkoff are personally profiting from a platform that investigators say has helped Iran evade the sanctions the US is supposed to be enforcing.

A new report from the Anti-Corruption Data Collective finds that political markets on Polymarket, despite making up just 4% of all markets, account for over a third of total trading volume and show disproportionately high signs of insider trading. In particular, they examine “longshot bets” — bets of $2,500 or more on shares trading at <35¢ — and find military and defense markets to be the starkest outlier, with such bets succeeding at a rate of 52%. This is far above what the market would predict, and winning bets cluster suspiciously in the final hours before resolution.

In the news

Mother Jones published an article about the Trump family’s World Liberty Financial project, where I’m quoted discussing its recent choice to borrow against its $WLFI treasury.

I’m quoted in a New Republic piece about media outlets increasingly integrating prediction markets into their platforms and, sometimes, the reporting itself.

I also made an extremely brief cameo in a Good Morning America segment about the US soldier who was arrested for his Venezuela-related prediction markets bets.

That's all for now, folks. Until next time,

– Molly White

Have information? Send tips (no PR) to molly0xfff.07 on Signal or molly@mollywhite.net (PGP).

I have disclosures for my work and writing pertaining to cryptocurrencies.

Footnotes

Sun does not explain in the lawsuit why World Liberty would be upset that he spent $100 million to purchase the $TRUMP memecoin — the proceeds of which also benefit Trump and his family — other than to note that the token is “sold by a different Trump-backed project”. The two projects do operate rather separately, as illustrated by an amusing dust-up back in June 2025. ↩

It’s a bit of a bold choice to use an alleged connection to Jeffrey Epstein as evidence of poor character when you’re suing a project co-founded by President Trump. ↩

Anyone else remember when crypto was supposed to be trustless? Just me? ↩

The SEC’s investigation into Gemini that was dropped in February 2025 is separate from the agency’s lawsuit against Gemini, which was dismissed with prejudice at the SEC’s request in January 2026 [I100]. ↩

References

“Crypto is at bottom of U.S. voters' priorities heading into elections, CoinDesk survey shows”, CoinDesk and CoinDesk-provided poll data. ↩

Complaint filed on May 5, 2026. Document #1 in Sun v. World Liberty Financial. ↩

Complaint filed on May 4, 2026. Filing #247349201 in World Liberty Financial v. Sun. ↩

Notice of pendency of other action or proceeding filed on May 5, 2026. Document #35 in Sun v. World Liberty Financial. ↩

“Trump’s crypto dinner cost over $1 million per seat on average”, NBC News. ↩

“Inside Trump’s Meme Coin Bash: Foreign Guests, Iran War Riffs, and Mar-a-Lago Charm”, Decrypt. ↩

24/48 hour report of independent expenditures (Schedule E) filed by the Fellowship PAC on April 21, 2026. ↩

“Scoop: GOP called Howard Lutnick to reverse crypto PAC's Texas move”, Axios. ↩

Amended 24/48 hour report of independent expenditures (Schedule E) filed by the Fellowship PAC on April 24, 2026. ↩

“Voter Perceptions & Support for CLARITY ACT Survey”, HarrisX. ↩

Indictment filed on April 23, 2026. Document #1 in US v. Van Dyke. ↩

Complaint filed on April 23, 2026. Document #1 in CFTC v. Van Dyke. ↩

“Trump Walks Back Prediction Market Criticism, Says 'Smart People' He Knows Like Them”, Decrypt. ↩

“U.S. senators won't be weighing in on prediction markets bets after banning themselves”, CoinDesk. ↩

Motion to vacate final judgment and dismiss complaint filed on May 4, 2026. Document #62 in SEC v. Bittrex. ↩

“CFTC's AI will review U.S. crypto registration applications, chairman tells CoinDesk”, CoinDesk. ↩

Stipulated order for permanent injunction, monetary judgment, and other relief against Alexander Mashinsky filed on April 28, 2026. Document #143 in FTC v. Celsius Network. ↩

“White House targets July 4 for Clarity Act passage, says crypto adviser Patrick Witt”, CoinDesk. ↩

“'Clarity Act will pass this summer': Coinbase CLO Grewal backs stablecoin compromise, urges banks to accept deal”, The Block. ↩

“Banking Trades Statement on Crypto Market Structure Yield Language”, American Bankers Association, Bank Policy Institute, Consumer Bankers Association, Financial Services Forum and Independent Community Bankers of America. ↩

“Crypto bill won't move without a ban on officials' industry ties, says U.S. Senator Gillibrand”, CoinDesk. ↩

“Tennessee just became the second state to ban 'crypto ATMs'. Here's why”, The Tennessean. ↩

Chapter 2, Spring Economic Update 2026, Government of Canada. ↩

“Exclusive: Nigel Farage was given undisclosed £5m by crypto billionaire in 2024”, The Guardian. ↩